Let’s live wealthy wise with this Simply Monthly Budget. Your journey to generational wealth begins today!

This tool will allow you to quickly visualize your monthly spending. You can also compare your actual spending to an ideal budget.

If you haven’t already downloaded the budget, you can find it here.

The spreadsheet is color-coded for your convenience. White means you should input data, red means you should leave it alone. Some of the red squares contain formulas that can get ruined if you play around with them too much.

The table is pre-filled with an income of $70,000, or ~$61,000 take-home pay.

Step 1:

Update the year if needed.

You can change between months using the tabs at the bottom of the spreadsheet.

You can either reuse the sheets monthly or copy the table every month.

Making a copy is easy:

- Right-click any tab

- Select move-or-copy

- Select where to place the new tab (usually at the end)

- Tick the “Create a copy” box.

Step 2:

Update your savings goal. Examples include an emergency fund, house downpayment, student loan balance, etc… This should be the primary bucket your extra cash is going into – and also your primary motivator!

Update your progress each month by inputting the amount you’ve saved toward your goal – and rejoice! This is proof of your hard work.

Step 3:

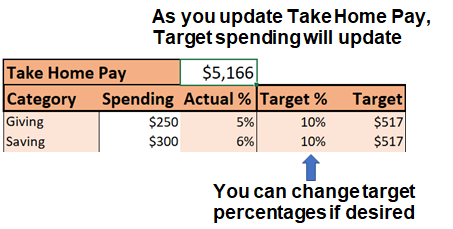

Determine your monthly income as take-home pay. That is, how much of your income is getting deposited into your bank account, available for use. This means you are ignoring what you’ve already paid in taxes, medical insurance, and job-based retirement savings which are automatically taken out of your paycheck. These tax-preferred savings are a bedrock of your savings plan and therefore off-limits for your spending plan. You will notice that as you change monthly income, the target dollar amounts will change but the percentages will stay the same.

An estimate is ok here. If your income is variable make a reasonable guess for that month. The important thing is to get your plan on paper to see any problem areas hampering your progress towards your financial goals. You can always update your income as the checks come in, you will get more accurate the more attention you pay to this.

Step 4:

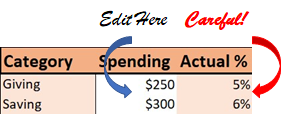

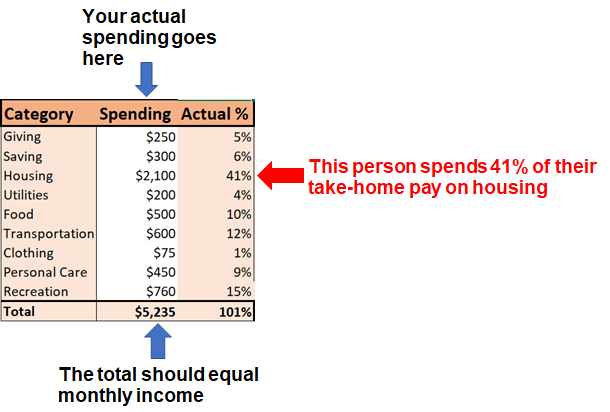

Enter your own spending per category in column C. This is where the real magic happens. You should be able to quickly identify any problem categories (mine is typically food). You can also compare your values against the hypothetical ideal budget in the middle section.

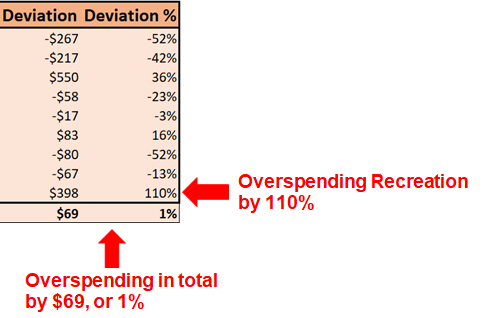

The final section calculates your spending’s deviation from our ideal budget. A negative value means you’re spending less than we allotted, and a positive number means you’re overspending your target. The last line (Total deviation) is extremely important. It tells you how much you are overspending your monthly takehome, or preferable, how much additional cash you can save toward your current goal!

Notes on Categories:

Giving: Yes, you read this right – you should be giving at LEAST 10% of your take-home to charities of your choice. Not only will you be helping to make the world a better place, but your generosity will also be edifying for you and the recipient.

“We make a living by what we get, but we make a life by what we give.”

Winston Churchill

Saving: This category is how you pay yourself first. Don’t include longterm savings such as your 401k here, as those shouldn’t be changed on a month to month basis. This category is more about working towards life goals. Once your emergency fund is complete, this category will be for things like saving to replace a vehicle – or a trip to Europe!

Housing: Remember to add purchases (such as furniture) and repairs to housing, not just your mortgage or rent.

Utilities: Make sure you’re accounting for all services: water, electric, gas, phone payments. Entertainment like cable and streaming services (Netflix) belong in the more discretionary recreation category.

Food: This includes restaurant and grocery spending. You can choose to move some or all of your restaurant spending to recreation.

Transportation: This is how much you’re paying to travel, whether for work or play. Include car payments, car repairs, fuel, taxi/rideshares, bus tickets, etc.

Clothing: If you don’t plan on buying any clothing for a particular month, consider putting this cash away. After several months of saving you can have a shopping spree! A side benefit of this is that you will always have an earmarked pile of cash to take advantage of inevitable sales and good deals.

Personal Care: This includes all the services and items you use to make yourself presentable. Hair cuts, shaving supplies, makeup, cleaning products, etc. This should also include any regular/recurring medical costs, such as a monthly prescription. Unusual medical costs will typically come from your emergency fund, although if you can swing it from this category all the better!

Recreation: Don’t fall into the trap of believing you’re not going to spend any money on recreation. All of us need to have activities and hobbies outside of work to be well-rounded, productive individuals. The purpose of budgeting is NOT to guilt you into miserly hoarding. A well-crafted budget will give you the freedom to splurge because you will know for a fact how much flexibility you have for things like an impromptu beach trip. It will feel a lot better to hand over that $200 for a nice beach condo if you’ve already budgeted $500 of “play money.”

Has this budgeting tool been helpful to you? Do you have issues or suggestions? Please let me know by posting a comment below!